By Peter Ip

THIS scribbler is an economist, otherwise known as ŌĆ£dismal scientistŌĆØ, by education and training as well as profession and career. My ingrained instinct is, therefore, to be sombre and lugubrious. I have also been compiling annual reviews and outlooks for Hong KongŌĆÖs jewellery industry since time immemorial (I jest: it is more like the better part of a decade). Not in recent memory can I recall captioning my brainchildren so confidently and rosily as above. Perhaps I should have hedged myself and tagged ŌĆ£Fingers CrossedŌĆØ at the end of the title. But, as they say, ŌĆ£nothing ventured, nothing gainedŌĆØ.

Better economies, better jewellery sales

The reason why, prima facie, I might have come across as gung-ho is that I set considerable store by the proposition that the better that economies near and far perform, the better will be our jewellersŌĆÖ sales, both at home and abroad. Since the global financial crisis erupted five years ago, followed by the Great Recession, the world economy has been muddling along, almost at all times failing to fire on all cylinders between and among different economies and sporting only isolated pockets of strength within any economy attempting a comeback.

Twenty fourteen promises to be noticeably different ŌĆō and not before time. In the all-important US economy, the worldŌĆÖs largest, the recovery has been variously described as anaemic, faltering, lacklustre and so forth. In the new year due to begin 1 January, however, it holds out hopes of being relatively inspiring, though given its likely continued subpar showing by historical standards, the emphasis should be more on ŌĆ£relativelyŌĆØ than ŌĆ£inspiringŌĆØ.

The transmission mechanism of prolonged quantitative easing (QE) ŌĆō massive purchases of government securities by the nationŌĆÖs central bank, the Federal Reserve ŌĆō on the economy remains to be more fully probed and understood. But, as QE boosts asset prices ŌĆō from stocks to bonds to houses to art and antiques ŌĆō it has indubitably resulted in a positive wealth effect that is supportive of consumer confidence and personal consumption expenditure. More importantly, deleveraging in AmericaŌĆÖs private sector has been unfolding steadily and gone further than similar processes in other advanced industrial countries.

Europe and Japan: Welcome aboard the recovery bandwagon

And the United States does not seem to be the ŌĆ£oasis of prosperityŌĆØ that former Fed chairman Alan Greenspan referred to in 1999, for its counterparts in the West appear increasingly to be jumping on the bandwagon heading for recovery as its destination. Thus, having contracted for six quarters running, the euro zone finally forayed into positive territory in the second quarter of this year; and the prognosis for 2014 is improving. European Central Bank president Mario DraghiŌĆÖs pledge ŌĆ£to do whatever it takesŌĆØ to maintain the intactness of the ContinentŌĆÖs single currency has wrought wonders in terms of order and stability as well as confidence.

Even Japan, putatively to have lost not one decade but two (and counting), is currently showing tentative but tantalising green shoots of recovery as Abenomics gradually come on stream and bring rejuvenating effects to bear on the Japanese economy. Inflation targeting, QE Japanese-style, fiscal activism and structural reforms together constitute the bedrock of the ambitious policies of Prime Minister Shinzo Abe, who is pursuing them with a vehemence and determination that are quite unheard of since when Junichiro Koizumi was in the driverŌĆÖs seat between 2001 and 2006.

ChinaŌĆÖs is a soft landing ŌĆō fingers crossed

More importantly, talk and angst of a hard landing for planet earthŌĆÖs second-largest economy ŌĆō that of our motherlandŌĆÖs ŌĆō have largely dissipated or at least been shelved. There is no doubt that ChinaŌĆÖs economy still has problems galore and that it has conceivably glided to a lower growth range and trajectory. Nevertheless, rebalancing in favour of consumption is taking place slowly, gradually and, on current indications, steadily, partly as a result of circumstances and partly thanks to the deliberate intent of government policy. Thus far into his new position as premier, Li Keqiang has inspired with his blend of targeted stimulus and structural reforms (Likonomics for short).

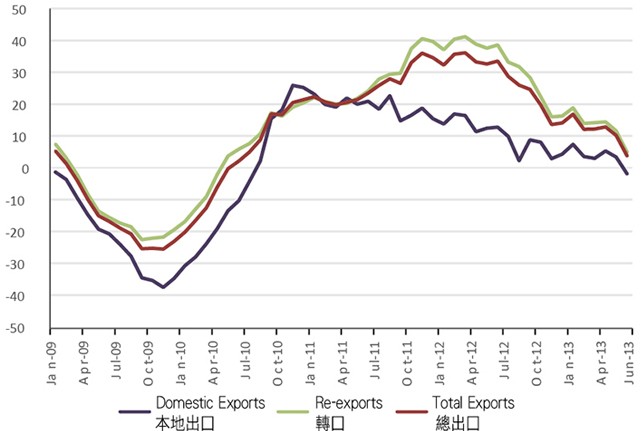

From the foregoing, I trust my readers will agree when I say that there is some ground for hopefulness about the 2014 prospects for Hong Kong special administrative regionŌĆÖs jewellery shipments overseas. And if that happy scenario does play out, it will stand in stark contrast to developments thus far in 2013: in the first eight months of this year, the value of total jewellery exports rose 6.7 percent over the same 2012 period, during which it soared 21.5 percent on the same basis. Within total exports, domestic exports eased 0.3 percent ŌĆō even worse than the minuscule 1.4 percent gain notched in the eight months ended August 2012 ŌĆō while the comparable figures for re-exports were 8.4 percent versus the 2012 periodŌĆÖs 26.4 percent.

Optimism? Yea; but caution too

I hasten to add that while some optimism can be entertained about next yearŌĆÖs jewellery export prospects, caution is still warranted as nothing has been signed, sealed and delivered. In the United States, politics, dominated by inter-party wrangling between the Republicans and the Democrats, is the gravest threat to sustained economic recovery. Ideological struggle, budgetary impasse, debt limit and potential default, government shutdown and the healthcare imbroglio all hang over the economy like swords of Damocles, with any one of them capable of bringing about debilitating fiscal retrenchment.

Meanwhile, in Europe, the nascent recovery has yet to find its footing. The unsettled political scene in Germany may yet bring strange bedfellows together but may also result in policies that are too German-centric for the good of the euro zone as a whole. Across the seas, in Japan, while the four ŌĆ£arrowsŌĆØ of Abenomics promise to be potent weapons of mass rejuvenation, the worry lingers that structural reforms that are positive from a long-term point of view could, if launched too hastily and extensively, undermine growth that is sorely needed in the short to medium term. As well, the renewed strength of the yen ŌĆō thanks in no small measure to dollar weakness ŌĆō could militate against reflation, corporate profits and economic activity again.

Beware of austerity China-style

At the outset of 2013, the single biggest worry about the Chinese economy is what looked back then like a probable hard landing, featuring a growth rate in the real gross domestic product with a five or six in front of the decimal point, inflation in excess of 4% and complete with a full-blown financial crisis. Now, as noted above, those worries have subsided. They may yet return, however, particularly if local public-sector debt, already reported to be in the trillions of renminbi, should turn out to be significantly bigger than consensus estimates. Problems may be accentuated if, among other reasons, overcapacity and idle infrastructure, coupled with a tighter-than-expected monetary stance as the residential market heats up anew, should turn the screws up.

Of course, even if the MainlandŌĆÖs economy manages to stave off the worst thinkable, a slower growth range is now but a foregone conclusion. Amidst a curtailment of loan growth and an uncompetitive exchange rate, it may not provide much of a fillip for luxury, including jewellery. Renaissance Capital (RC) probably sums things up best:

China is a key market for the luxury goods industry due to Chinese consumersŌĆÖ affinity for these products. The slowdown in economic activity, harsh measures introduced to curb the housing market (higher interest rates and deposit requirements) and a drive to curb public-sector corruption have led to softening trends in sales of luxury goods growth since the second half of 2012.

As part and parcel of the anti-corruption drive, the powers that be are cracking down on lavish corporate entertainment and gifting practices (and one hastens to add that this is all to the good of the country). The anti-corruption campaign, in turn, is adjunct to a rigorous effort on the part of Zhongnanhai to promote conservation and frugality as a lifestyle. All told, RC reckons that the effect can be seen most strongly in wine and jewellery.

Domestic sales still going strong

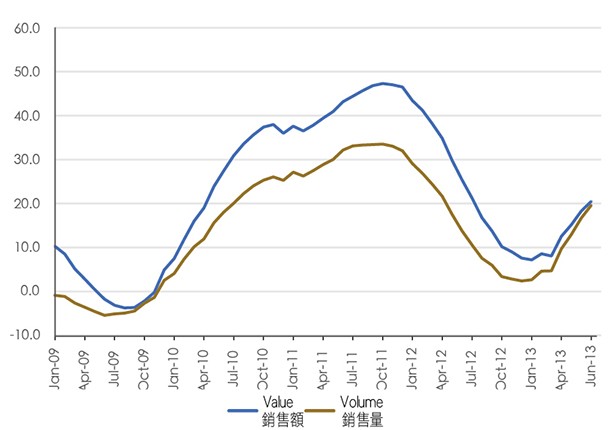

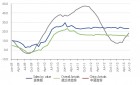

The foregoing having been noted and given that Mainland China and Hong Kong are akin to lips and teeth (that is, one cannot do without the other), it may come as something of a surprise that within HKSAR, retail sales of jewellery, watches, clocks and valuable gifts have been doing remarkably well in 2013 to date (Figure 2). In the first eight months of this year, such retail sales leapt by 30.4 percent by value and 30.5 percent by volume as prices remained broadly stable; the comparable figures for the corresponding 2012 period were 8.3 percent and 1.3 percent, respectively.

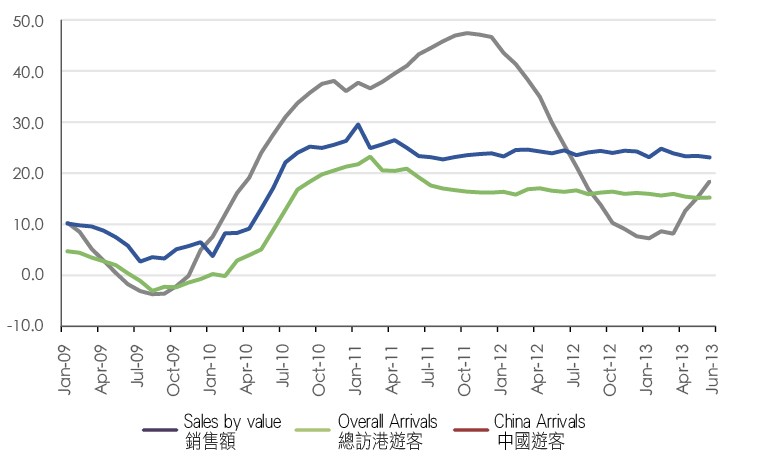

There can be no doubt that domestic sales of jewellery have been helped immensely by tourist arrivals, foremost those hailing from north of the border and not least those visiting HKSAR by way of the Individual Visitor Scheme that has spread to theMainlandŌĆÖs inland regions.

But already there have been signs of consolidation ŌĆō even slowdown ŌĆō in the growth rate of visitor arrivals. Thus, in the eight months ended August, overall tourist arrivals grew 12.6 percent over the same 2012 period. That was respectable by most standards but represented a retreat from the year-ago outturn of 16 percent. Chinese visitor arrivals continued to rise at a pacesetting clip ŌĆō of 18.8 percent - but again this denoted a climbdown compared with 23.4 percent in the first eight months of 2012. That said, China still accounted for 75 percent-plus of total tourist arrivals. Mainland Chinese visitors are thus pivotal for the performance and prospects of HKŌĆÖs tourism industry, comprising ŌĆō as said ŌĆō jewellery.

The China connection: too important to be neglected

By one press-reported estimate, each of these visitors spends some HK$8,500 during their sojourn in HKSAR, one-third of which is expended on jewellery. For what it is worth, my personal hunch is that the portion accounted for by jewellery is larger ŌĆō and would continue higher. The reason is that as our motherlandŌĆÖs economic growth and development becomes more widespread territorially and inclusive society-wise than hitherto has been the case, there will be more would-be jewellery purchasers and owners; the pent-up demand, it can be believed, is formidable.

As Mainland tourists skimp on food and lodging (as they reportedly have already been doing), they are likely to splurge to the hilt on the traditional status symbols of watches and jewellery. Besides awaiting their arrival, another potentially rewarding way of capitalising on Chinese consumersŌĆÖ immense and expanding appetite for jewellery is to gear up for the increasingly important and popular digital trade of luxury in general and jewellery in particular. Hong KongŌĆÖs jewellery practitioners would be well advised to consider setting up their own websites and related portals within China itself as this would facilitate electronic access by Mainland-based buyers and avert possible delays and inaccessibility.

← Back