┬Ā

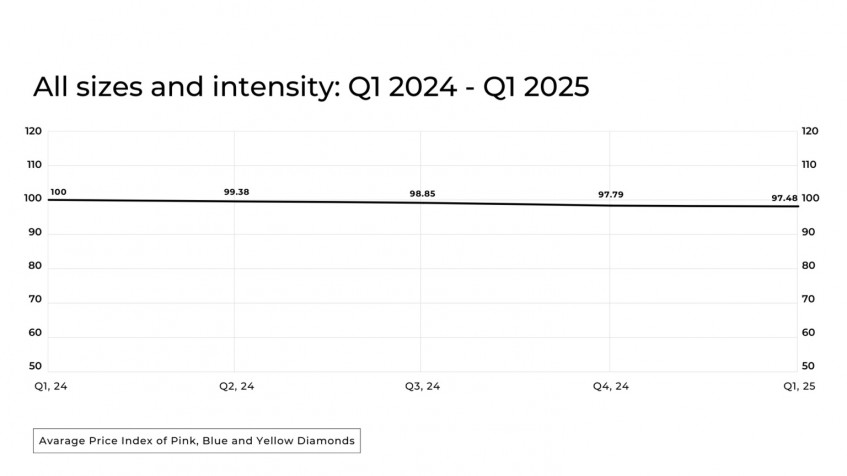

The Fancy Color Research Foundation (FCRF) has announced the first quarter results of the Fancy Color Diamond Index (FCDI) on 23 April 2025. The overall FCDI recorded a modest decline of 0.3 percent in Q1 2025, compared with the more significant previous quarter's price drop of 1.1 percent.┬Ā

┬Ā

Over the trailing 12 months, the index has declined only by 2.5 percent, reflecting a broader softening across several categories. FCRF said that signs of market stabilisation are becoming evident.

┬Ā

According to FCRF, during the final weeks of Q1 2025, the market witnessed growing concern over proposed United StatesŌĆÖ tariff policies and shifting global trade dynamics. While this report does not explicitly account for macroeconomic developments outside of pricing data, it is important to recognise the broader context. ŌĆ£The flip side of the coin is that these tariffs may create a shortage of colour diamonds in the US market, which could further drive up prices. Additionally, with all colour diamonds now required to go through the GIA laboratory in Hong Kong, a slower supply chain is anticipated. This index reflects Q1 activity as recorded in the global trading centres, and we will continue to monitor any effects that may emerge in the quarters ahead,ŌĆØ said the FCRF.┬Ā

┬Ā

One of the most notable developments this quarter is the halt in price erosion across several sub-categories, particularly in the high-saturation segment. Among these, fancy vivid yellow diamonds (all sizes) reversed a 2.2-percent decline in Q4 2024 to a flat performance (0.0 percent) in Q1 2025. While this isn't a full recovery, it does signal growing support at the lower end of the pricing curve, hinting at renewed interest or a slowdown in selling pressure for this vivid sub-category.┬Ā

┬Ā

Although some other sizes continued to decline, the rate of depreciation has generally eased, suggesting the possible establishment of a price floor in the market. ŌĆ£While the headline number shows a mild quarterly decline, the underlying data tells a more optimistic story: certain categories have stabilised, and volatility across others has significantly slowed, which may set the stage for a potential rebound in select categories throughout upcoming quarters,ŌĆØ FCRF summarised.┬Ā

┬Ā

The Pink diamond segment remained the most stable among the three primary colour categories in Q1 2025, registering a minimal quarterly decline of 0.1 percent. This follows a similar pattern from Q4 2024 (ŌĆō0.8 percent), indicating that pink diamonds have weathered broader market pressures with relative resilience. On a 12-month basis, pink diamonds are down 1.2 percent, a comparatively modest decline when measured against the deeper reductions seen in the yellow and blue categories.┬Ā

┬Ā

Blue diamonds posted a moderate decline of 0.5 percent in Q1 2025, following a 0.3-percent decrease in Q4 2024. Over the last 12 months, the category has declined by 1.9 percent, placing it between the pink and yellow categories in terms of relative performance.┬Ā

┬Ā

The yellow diamond segment in Q1 2025 saw a price decrease of 0.7 percent, which follows a 2.2-percent drop in Q4 2024. Over the 12-month period, yellow diamonds are down 6.1 percent. Notably, four of the five largest price decreases in Q1 occurred in yellow diamonds. The most affected was the 3-carat fancy intense yellow category, which dropped 3.00 percent, followed closely by the 10-carat fancy yellow (ŌĆō2.60 percent), 2-carat fancy intense yellow (ŌĆō2.50 percent), and 1-carat fancy intense yellow (ŌĆō2.20 percent). (Photo courtesy: FCRF)

┬Ā

09-05-2025

┬Ā

← Back